Interest rates will stay higher for longer

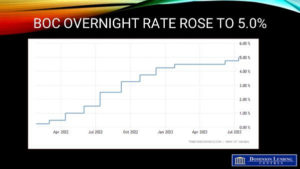

The Bank of Canada increased the overnight policy rate by 25 basis points this morning to 5.0%, its highest level since March 2001. Never before has a policy action been so widely expected. Still, the Bank’s detailed outlook in the July Monetary Policy Report (MPR) suggests stronger growth and a longer trajectory to reach the 2% inflation target. The Bank of Canada believes the economy is still in excess demand and that growth will continue stronger than expected, supported by tight labour markets, the high level of accumulated household savings, and rapid population growth. “Newcomers to Canada are entering the labour force, easing the labour shortage. But at the same time, they add to consumer spending and demand for housing.”

The Bank forecasts GDP growth to average 1.0% through the middle of next year–a soft landing in the economy. “This means the economy moves into modest excess supply in early 2024, and this should relieve price pressures. CPI inflation is forecast to remain about 3% for the next year, before declining gradually to the 2% target in the middle of 2025.” This is about six months later than the Bank expected in April. This means that high-interest rates remain higher for longer.

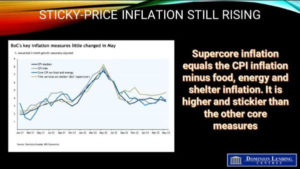

While Canadian inflation has fallen quickly, much of the downward momentum has come from lower energy prices and base-year effects as large price increases last year fall out of the year-over-year inflation calculation. We are still seeing large price increases in a wide range of goods and services. Our measures of core inflation—which we use to gauge underlying inflationary pressures—have come down, but not as much as we expected.

There continue to be large price increases in a wide range of goods and services. Measures of core inflation have come down, but by less than expected (see chart below). One measure of core inflation–which removes food, energy and shelter prices, remains elevated and will likely continue to be sticky.

To remove base effects, the Bank looks at three-month rates of core inflation, which have remained at 3.5% to 4.0% since September 2022, almost a percentage point above the Bank’s expectations at the beginning of this year.

In addition, labour markets remain tight. Although the jobless rate has risen to 5.4%, that is still low by historical standards. The unemployment rate was at 5.7% when the pandemic began, which was considered close to full employment at the time. Job gains have been robust, with about 290,000 net new jobs created in the first six months of 2023. Many new entrants to the labour market have been hired quickly, and wage growth has been about 4% to 5%.

Bottom Line

As always, the next steps by the Bank of Canada will be data-dependent. Interest rates will remain higher for longer if the Bank is correct that inflation will not reach its 2% target until 2025. We also cannot rule out more rate hikes in the future. This morning, the US inflation data for June were released, showing a marked decline from 4% in May to 3% in June. Markets rallied worldwide, taking Canadian bond yields down despite the BoC tightening. The hardship caused by the continued rise in mortgage rates is already evident. OSFI recently announced the possibility of higher capital requirements for federally insured financial institutions on mortgages with loan-to-value ratios above 65% that have unusually high amortizations. This proposal is now out for consultation. It seems OSFI and the federal consumer watchdog are working at cross purposes.

https://sherrycooper.com/category/articles/